How Blockchain is Impacting Our Life & Make Our World Better

Blockchains are the future; that much is certain. Even right now, it’s making major changes all over the world. Don’t say that’s debatable, because I’ll just plug my ears and ignore you.

I’m glad you aren’t arguing with me.

Let’s get on with this, shall we?

Before I tell you why it’s so awesome, I’ve got to make sure you actually know what an blockchain is.

Ever heard of cryptocurrency?

That’s a currency – a digital currency – which involves the use of encryption techniques for the regulation of the generation of units of currency and the verification of the transfer of funds.

And get this: its operation is not in any way dependent on a central bank.

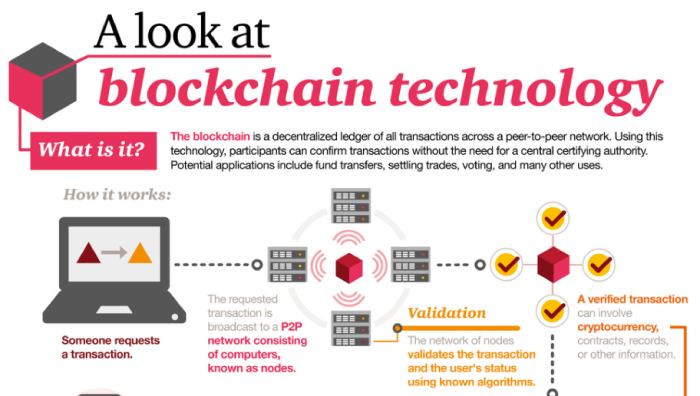

That’s where blockchains come in. They’re a whole lot cooler. They’re digitalized, decentralized. A blockchain is pretty much a ledger of all transactions made using cryptocurrency.

It’s used for verification, creating indelible records. The blockchain, in short, is a bank that isn’t like the average bank you see these days. And it’s got huge benefits.

What are the Benefits of Blockchains?

1. More Affordable and Reliable Remittance Payments

What’s remittance?

It’s basically a money transfer between a foreign worker and someone in their country of origin.

The use of blockchain has brought great benefits in this area of the financial industry by attacking many of its problems.

Take fraud for example. It happens to be a huge problem faced by the financial industry. With blockchain, this problem can be overcome.

The technology presents a challenge for fraudsters and hackers[3]. When transactions are fixed, it is quite easy to detect fraudulent attempts to change them.

The blockchain prevents forgery and destruction of previous transactions by protecting the links between them through cryptograph.

Nowadays, without the use of blockchain technology, cross-border payments are made through correspondent banks or providers of money transfer; there’s also no central clearing system for making these transactions.

And there’s the other problem. The transactions can only be done during bank hours. I’m sure you agree that that totally sucks.

But what happens when you use blockchain technology?

You see, the fact that there’s a public ledger that involves the recording of every transaction occurring on the network guarantees that there will be a maintenance of identical copied of transaction records, on the computers of each network.

This means that all the parties involved in the transactions will are able to review and record prior and new entries respectively.

With the use of blockchain technology, it is possible for the sender and the recipient of the money being transferred to locate their money. The fact that there aren’t any intermediaries makes for a quicker transfer process.

2. Philanthropy/Charitable Donations

It’s no news that charity organizations manage a lot of money and have to do a lot of research, not to mention go through complex accounting processes.

With blockchain technology, everything’s a breeze.

Let’s begin with the use of “smart contracts”. Traditional contracts require a middleman, such as a legal firm. Donations through contract must involve this third party to ensure that there is no fraud or manipulation.

With blockchain technology, are third parties still required?

Pshaw!

Blockchains have the ability to contain a lot of data, which includes contracts. With the use of “smart contracts”, whose protocols enforce performance, there will be no need for middlemen.

Payment will be done based on milestones which are to be met by users; when certain conditions are met, transactions can be made. Smart contracts don’t “forget” agreements, and this allows for effective, electronic enforcement.

They create escrows which cannot be manipulated by a single user. This effectively takes care of the waning trust that people often have in charities.

3. Banking The Unbanked

Not everyone has a bank account. It sounds strange, doesn’t it?

Well, it’s quite true. Many people aren’t able to use banks to meet their everyday financial needs.

All those benefits you get from owning a bank account? They don’t have them.

Now, here’s where the problem lies. Although owning a bank account comes with lots of advantages like security and convenience, not everyone can enjoy them, because not everybody owns a bank account.

How does blockchain solve this problem?

Well, blockchain technology allows the unbanked to create financial alternatives[2] efficiently. They acquire digital identities which they can use in their banking.

Also, it is possible for property rights to be moved onto a blockchain, which allows low-income individuals to get into formal networks of information and use their property as collateral.

Remittance through blockchain is quite effective, an added advantage for low-income individuals.

For them, blockchain is nothing short of Nirvana.

4. ICOs for Social Good

Initial Coin Offerings, also known as ICOs, have nothing to do with the kind of coins you can put in your pocket. They have to do with the use of cryptocurrencies for funding and can be used as capital for startup companies.

ICOs give opportunities to companies from which society can reap benefits. For example, Impak Coin has over $1 million, which will be used for the funding of businesses which will bring both financial and social benefits.

The CEO of Impak Coin, Paul Allard, believes that ICOs offer[1] an opportunity for socially beneficial companies to attain more capital, and also to end the dominance by traditional players in startup financing.

Allard desires to create a bigger “ecosystem” of companies as well as investors which aren’t traditionally financial.

It’s wonderful, isn’t It?

I mean, blockchains cut across pretty much every aspect of our lives, from security to charity and banking.

Read Next: Blockchain Whispers: The #1 Best Telegram Channel for Crypto Trading Signals

They remove the need for third parties, middlemen, which can easily be influenced by either of the two parties originally involved in agreements.

They make it impossible for actions to be taken without the consent of all parties involved, thus many problems are avoided.

Policies are enforced with speed and precision, fraud and corruption are easily detected and can be checked, and everyone goes home happy – except criminals, of course. They go to jail.

Feature Image: Shutterstock.com

In Post Image: http://cryptographybuzz.com, cdn.cnn.com/ & Shutterstock.com

References

[2] https://medium.com/@Borderless/banking-the-unbanked-an-opportunity-for-a-blockchain-powered-financial-ecosystem-90a571a8a19e

[3] https://www.forbes.com/sites/danielnewman/2018/04/17/3-ways-blockchain-can-help-combat-fraud/#3b08f06992a4

Disclaimer

The writer’s views are expressed as a personal opinion and are for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.More Posts

Regulatory challenges of Security Tokens

Photo by Markus Spiske on Unsplash We like to talk about digital coins and the tokenization of products services and pr...

BNB Reaches New Highs After Binance Launches Own DEX And Blockchain Network

Binance announced that they launched testnet of Binance Chain. Shutterstock Images Binance, one of the largest and most...

Cosmic Messages: Allows Bitcoin Holders to Send Messages into Space

Cosmic Messages to allow communication into space. NASA/JPL Images By replacing Blockchain’s transmission via satel...

Senate Bill 5638: What Does the New “Blockchain Bill” Mean for Washington State?

Washington Electronic Authentication Act would be revised by Senate Bill 5638 (SB 5638). Shutterstock Images On Janu...

{kind=link}